Copaymentsset quantities that you spend for doctor check outs, prescription drugs, or check outs to an immediate care facilitymay not count towards your deductible for the year. Co-payments are not to be confused with coinsurance, which is the quantity you spend for medical services once you have actually fulfilled your deductible and your plan begins to pay.

In 2018, the typical health insurance coverage deductible for Americans covered by an employer's healthcare plan was $1,350. That applies to single-person protection and is the minimum threshold for a high deductible health insurance (HDHP). These plans bring greater deductibles, but they provide a compromise in the kind a health cost savings account (HSA) that can be used to save for future health care expenses on a tax-advantaged basis - how much is an eye exam without insurance.

To certify as a high deductible health insurance, the minimum deductible for single protection should be $1,350 or higher for 2019, or $2,700 or greater for household protection. The minimum deductible for family protection to qualify as a high deductible health insurance in 2019. The minimum deductible for single coverage is $1,350.

If you don't see the medical professional that frequently, it's possible that you might not meet your plan's deductible for the year based upon what you invest expense for healthcare. In that scenario, you 'd need to consider whether it would make more sense to choose a strategy with a greater premium to get a lower deductible or vice versa.

Depending upon how their strategy is structured, it might be basically economical to go from single to family protection. If you're getting medical insurance through the federal market, compare the different tiers to identify which one is best. The 4 tiers offered are Bronze, Silver, Gold, and Platinum.

At the other end of the spectrum, a Platinum strategy would provide the most coverage for health care plus the most affordable deductible. That could be excellent if you have higher costs for things like routine care, specialists, or prescription drugs. The trade-off is that Platinum strategies will be most pricey with regard to premiums.

How Long Can You Stay On Parents Insurance Can Be Fun For Everyone

You need to register at the Silver level or greater, but if a cost-sharing reduction is available, this can discount the quantity you pay for your deductible, co-payments, and coinsurance. i need surgery and have no insurance where can i get help. If you do not believe you'll meet the plan's deductible for the year, it's possible to work out lower rates for care if you choose to self-pay rather of utilizing your insurance coverage.

Your deductible belongs to your out-of-pocket optimum (or limitation). This is the most you'll pay during a policy duration for enabled amounts for covered healthcare services. Other cost-sharing elements that count toward hitting your out-of-pocket maximum: Repaired dollar amounts of covered health careusually when you receive the service.

You likely won't pay coinsurance, calculated as a percentage of shared costs between you and your health strategy, up until your deductible is fulfilled. Typical coinsurance varieties from 20 to 40% for the member, with your health strategy paying the rest. As soon as your deductible and coinsurance payments reach the quantity of your out-of-pocket limitation, your plan will pay 100% of allowed amounts for covered services the remainder of the strategy year.

In almost any area of your life, if you do not have a clear concept of your expenses, you may seem like you're not in control. But, when you get clear about all the costs, you feel in control, helping you make the right choices. To get a clear understanding of your health insurance costs, the initial step is to look at all the key types of expenses, not just obvious expenditures.

Less apparent expenses include the finance charge on your payment, windscreen wiper fluid and parking tickets. Let's take a look at obvious health insurance expenses and some examples. Your medical insurance plan premium is an obvious expense, and the majority of people pay it on a regular monthly basis. Your premium is the payment you make to your health insurance business that keeps your coverage active.

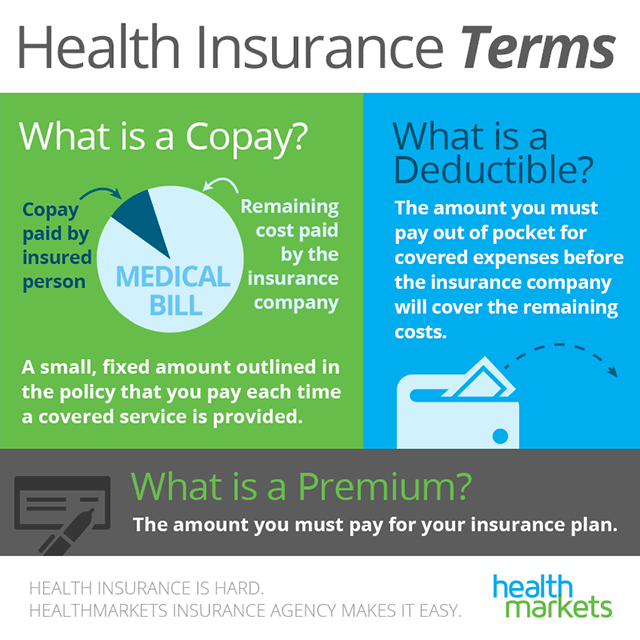

You may currently be familiar with a few of these terms. Here are quick definitions and simple examples. What is it? Here's an example ... Premium A premium is the quantity of cash charged by your insurance provider for the strategy you have actually chosen. It is normally paid on a regular monthly basis, however can be billed a number of methods.

The 25-Second Trick For How Long Can My Child Stay On My Health Insurance

You have actually researched rates and the health plan you have actually selected costs $175 each month, which is your premium. In order to keep your advantages active and the strategy in force, you'll require to pay your premium on time on a monthly basis. Deductible A deductible is a set quantity you have to pay every year toward your medical expenses prior to your insurance coverage company starts paying.

Your strategy has a $1,000 deductible. That implies you pay your own medical costs up to $1,000 for the year. Then, your insurance coverage kicks in. At the beginning of each year, you'll have to meet the deductible again. Coinsurance Coinsurance is the portion of your medical expense you show your insurance provider after you've paid your deductible.

You have an "80/20" plan. That indicates your insurance provider pays for 80 percent of your costs after you've fulfilled your deductible. You pay for 20 percent. Coinsurance is various and different from any copayment. Copayment (or "copay") Your copayment, or copay, is the flat fee you pay every time you go to the physician or fill a prescription.

Copays do not count towards your deductible. Let's state your strategy has a $20 copayment for regular doctor's visits. That suggests you have to pay $20 each time you go. Copayments are different than coinsurance. Like any kind of insurance coverage plan, there are some expenditures that might be partly covered, or not at all.

Less obvious expenses might include services offered by a physician or health center that is not part of your strategy's network, plan limitations for particular sort of care, such as a specific variety of check outs for physical treatment per advantage period, in addition to over the counter drugs. To help you find the right plan that fits your budget, appearance at both the obvious and less apparent expenditures you may expect to pay.

If you have various levels to pick from, choose the greatest deductible quantity that you can https://cruzdjuk135.wordpress.com/2021/12/22/what-is-marketplace-insurance-truths/ easily pay in a calendar year. Find out more about deductibles and how they impact your premium.. Price quote your total number of in-network physician's gos to you'll have in a year. Based upon a plan's copayment, include up your total cost - what is a premium in insurance.

What Is A Premium In Health Insurance Things To Know Before You Get This

Even plans with extensive drug coverage may have a copayment. Figure in oral, vision and any other routine and required take care of you and your household. If these expenses are high, you may desire to think about a strategy that covers these expenses. It's a little work, but taking a look at all expenses, not just the apparent ones, will help you discover the strategy you can afford.